Features

National Pension System (NPS) is a retirement benefit Scheme introduced by the Government of India to facilitate a regular income post retirement to all the subscribers. PFRDA (Pension Fund Regulatory and Development Authority) is the governing body for NPS.

Salient Features & Benefits

National Pension System (NPS) is based on unique Permanent Retirement Account Number (PRAN) which is allotted to every subscriber. In order to encourage savings, the Government of India has made the scheme reassuring from security point of view and has offered some attractive benefits for. NPS account holders.

An NPS Account offers the following benefits:

- Regulated: NPS is regulated by PFRDA (Pension fund regulator under Ministry of Finance, Govt. of India.) which ensures transparent norms governing the activities. NPS Trust ensures adherence to the guidelines through regular monitoring.

- Voluntary: It is a voluntary scheme for all citizens of India. You can invest any amount in your NPS account and at anytime.

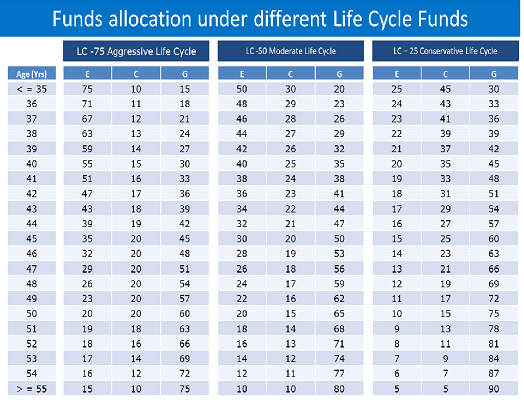

- Flexibility: You have the flexibility to select or change the POP (Point of Presence), investment pattern and fund manager. This ensures that you can optimize returns as per your comfort with various asset class (Equity, Corporate Bonds, Government Securities and Alternate Assets) and fund managers.

- Economical : NPS is one of the lowest cost investment products available.

- Portability: NPS account or PRAN will remain same irrespective of change in employment, city or state.

- Superannuation Fund transfer: NPS account holders can transfer their Superannuation funds to their NPS account without any tax implication. (Post approval from relevant authorities)

- Tax Benefits: NPS offers triple tax benefits which are as follows:

Tax benefits for Salaried Individual | Tax Benefits for Self Employed Individual |

Investment up to 10% of Salary (Basic + Dearness Allowance) routed through the Employer, is deductible from taxable income u/s 80CCD (2) of Income Tax Act, 1961 which is over and above Rs. 1.5 lakhs limit of section 80C under Old Tax Regime. Additionally, investment up to Rs.50,000 is deductible from taxable income u/s 80CCD (1B) of Income Tax Act, 1961 under Old Tax Regime. Employees opting for New Tax regime, can choose up to 14% of Salary (Basic + Dearness Allowance) routed through the Employer, is deductible from taxable income u/s 80CCD (2) Maximum limit of amount that can be claimed tax exempt is Rs. 7.5 lakh of employer contribution towards, NPS, PF and Superannuation all together. (Only available for Corporate NPS accounts). | You can claim tax exemption upto Rs. 50,000 under section 80CCD (1B). This benefit is over an above limit of Rs. 1,50,000 under section 80C. |

Please Note

Tax deductions u/s 80CCD (1) and 80CCD (1B) shall be available only if the taxpayer opts for old tax regime. Please consult your CA to know more about this.

Tax benefit under Section 80 CCD (2) can be availed in either of the tax regimes